The software market is large (more than 500 billion global market volume in 2022) and very heterogeneous. Trends such as the switch from on-premise to SaaS solutions, the entry of innovative competitors, and the digitalization of new industries and applications make the market an extremely dynamic environment. In the coming years, the integration of artificial intelligence – both in the creation and use of software – will further change the market and influence M&A activity in the market.

If the sale of a software company is sought, management and shareholders should understand exactly which specific aspects influence the company value, the approach in the sales process, and the likelihood of a sale.

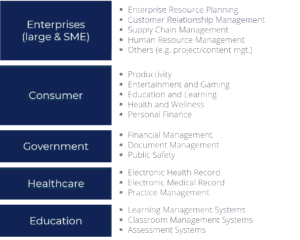

Types of software companies

So far, no good and non-overlapping classification of the software market has been established. We would somewhat simplify the market by dividing it according to user groups:

Software Segments and application examples

Software Segments and application examples

What factors influence the valuation of a software company

Company valuations are derived in practice using various methods. Although the company value is the price a buyer is willing to pay for the acquisition from an M&A perspective, it makes a lot of sense to think about a potential valuation or a valuation corridor before selling the company.

Typically, a company is valued based on EBITDA or revenue multiples. You can find a general overview of company valuation methods, including for software companies, here. Beyond such an individual company valuation, however, there are valuation drivers that particularly impact selling prices for companies in the software industry. We want to explain these in more detail below.

Revenue growth vs. profitability

Typically, in company valuations, particular attention is paid to a company’s profitability. The more attractive the market, the more the focus is on dynamic revenue growth. High revenue growth can set up very attractive business plans in many segments of the software industry – thus arguing for a much higher future company value.

This is particularly evident in companies that offer Software-as-a-Service (SaaS) solutions and generate annual or monthly recurring revenue. In the years until about mid-2022, high growth of SaaS companies was rewarded with very high valuations.

The level of valuations has significantly reduced in the following quarters, but SaaS companies can still expect above-average high valuations (compared to classic valuation approaches). However, entrepreneurs and investors can no longer assume that deficits in profitability will be compensated for by increasing valuations – always based on revenue.

The “Rule of 40” as a rule of thumb for the attractiveness of a SaaS provider

US investors Bessemer Venture Partners developed a rule of thumb for SaaS companies, the so-called Bessemer Efficiency Score (“Rule of 40”). The key figure evaluates the efficiency of revenue growth by relating growth and profitability: The sum of the revenue growth rate in % and free cash flow rate in % should not be below 40.

If a SaaS company grows by 60% in revenue in a year, then according to this rule a negative free cash flow rate of 20% would be acceptable. This is a somewhat striking simplification, but it clearly demonstrates the outstanding importance of growth in assessing software companies by buyers and investors.

The ratio of customer value and customer acquisition costs

Buyers and investors want to understand exactly how well a company’s business model works. For software companies, it makes sense to consider the so-called “Customer Life-time Value (CLTV)” and the “Customer Acquisition Costs (CAC)” and to put them in relation. The CLTV is the expected sum of the gross margin or contribution margin 1, which the company can earn with the customer during the entire duration of the customer relationship. The CAC are the sales costs to win this customer.

It is obvious that different magnitudes and ratios are important in enterprise and consumer software business. Enterprise software typically has higher absolute sales costs but also higher expected revenues. Consumer software is sold for lower prices and is based on different sales processes. The very important “churn rate” is included in the CLTV, i.e., the proportion of customers in a period who stop using the product.

The better the ratio of CLTV/CAC, the more attractive and scalable the business model, and the higher the company valuation will be.

Large markets enable high valuation

The total addressable market, the so-called “Total Addressable Market” (TAM) of the company to be divested, has – in principle – an important influence on the company value. For example, a technically brilliant software in a niche industry will be valued lower than a technically average, cross-industry software solution that can work a very large market.

But: In 99 out of 100 business plans, you will find huge numbers for the TAM and the SAM (the so-called “Service Addressable Market”). Buyers will hardly be dazzled by this in the M&A process. Although market size is important, the traction the company can demonstrate in the market is much more significant.

Company size has a strong impact on company valuation

Companies with higher revenues generally achieve higher company valuations than smaller companies. A larger company has achieved a solid market position with a notable market share, thereby proving the fundamental sustainability of its business model. If revenues are below 10 million Euros per year, a price discount must be expected when selling the company.

Very small companies regularly experience that large competitors are not interested in a takeover at all. Even if there is an interesting technology or a unique selling proposition. The company is then frankly not relevant for the larger market participant. Even with very smart technologies, we as M&A advisors have heard something like “interesting technology, but please get back to us when the company is ten times bigger”.

Customer relationships as value drivers

In every M&A process, the analysis of the customer relationships of the company to be sold is of particular importance: A good customer mix reduces the lump risk and thus also the risk of a bad investment by the buyer. In addition, future sales expectations can be derived from the duration, quality, and development of customer relationships.

Similarly, customer relationships can represent an asset. For example, a strategic investor can try to offer existing customers additional products and services after the transaction.

A good strategic fit increases the purchase price

The best valuation can be paid by a buyer who achieves synergy effects and strategic advantages through the acquisition. If there are cross- and upsell potentials, this will improve the underlying business plan for the buyer.

In the software industry, hybrid business models have increasingly emerged in recent years: Many of the large IT consulting firms like Accenture or Cognizant have acquired software companies to complement their personnel-dependent service with a scalable software product business and differentiate themselves in the competition.

What is important in addition to the company valuation when selling a software company?

Often, the goal in selling a company is to maximize the purchase price – we find it more appropriate to speak of optimization. The best result of a transaction allows the highest purchase price and the meeting or achieving of the seller’s most important side conditions and goals. Important points include, for example:

Purchase price tranches and options

Typical arrangements are the takeover of a majority with associated put/call options, good/bad leaver regulations, and performance-based purchase price adjustments or the payment of different purchase price tranches. These elements of a so-called share purchase agreement are of great economic importance to the sellers and must already be determined when agreeing on a preliminary contract, e.g. within the framework of a letter of intent.

Retention and expected duration of the team’s stay

Small and medium-sized software companies are often dependent on the know-how of the company founders or the core team. A buyer will therefore expect that the entrepreneurs will stay on board for a certain period of time after the sale is concluded. This directly influences the structure of a deal and is reflected in the contract. Typical periods range between two years (rather short) and five years (rather long).

The right company culture leads to a good deal for both sides

A soft but not to be underestimated point is the company culture of the buyer. The team has to develop the (formerly own) company together with the buyer for a few more years. It makes no sense to sell to a partner that the entrepreneurs believe will not be fun to work with or will operate in a fundamentally different atmosphere. The probability of achieving the earn-out targets is then much lower.

A good equity story leads to a good company valuation

The valuation and sale of a software company cannot follow a standard procedure. The differences are too great and the specific strengths and weaknesses of a company must be argued in a suitable way to optimize the result of the M&A process.

The value drivers shown above should be picked up in a suitable way and transferred into a consistent so-called “equity story”. That is the justification for a potentially attractive company value.

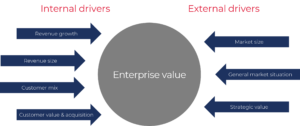

Drivers of enterprise value

The involvement of an experienced advisor enables negotiations at eye level

If you want to sell your software company, it is strongly recommended to involve a professional M&A advisor. On the buyer’s side, there are M&A experts whose daily business is to conduct company examinations and negotiations. Ensure a balanced power relationship by also involving a professional.

Experts at the interface of technology and transaction

The team at Quantum Partners has many years of experience at the intersection of high technologies and company transactions. We have supported software and IT companies in sales to strategic partners and financial investors. We are aware that each company and its position in the market is unique and requires an individual approach.

We aim to present your company as attractively as possible to as many interested parties as possible and to actually address all relevant parties. We approach this very consciously and never undifferentiated in the market.

About Quantum Partners

Quantum Partners is a corporate finance and M&A advisory firm specializing in software & business services, digital media & commerce, industrial technology, and cleantech & sustainability. From its office in Munich, Quantum Partners advises clients worldwide on the sale of companies, acquisitions, and financing.

Call us for a confidential exchange of ideas. We would be happy to discuss our approach, our industry expertise and references for our work with you.

Dr. Andreas Brinkrolf

Managing Director

brinkrolf@quantum-partners.de

+49 89 414144 355

FAQ: Valuation of software companies

Which key figures are most important when evaluating software companies?

Typically, ARR/MRR are important for measuring revenue, revenue growth, and gross margin. Depending on the business model (SaaS vs. license vs. usage), NRR/churn, CAC/payback, and net dollar retention may also be important.

Why can a SaaS company be valued very highly despite losses?

If the business model is intact, i.e., the unit economics are right (e.g., fast CAC payback, high gross margin) and retention is strong, today’s losses can be seen as an investment in growth. Buyers then pay for the expected future scaling of cash flows.

What role do NRR and churn play in company valuation?

NRR (Net Revenue Retention) shows whether revenue from existing customers is growing organically and is an important measure of upselling, pricing power, and customer loyalty. High churn indicates that customers are reducing their usage and that the software is apparently not delivering the expected value.

Which due diligence issues have the greatest impact on company valuation?

Due diligence involves intensive examination of issues that cannot be captured by individual KPIs but are nevertheless very important, such as revenue quality (type of contracts, termination rights, price increases), customer concentration, and product/technology risks (scalability, security, IP). The quality of the sales pipeline and potential dependencies on a small number of individuals are also analyzed and may lead to risk discounts in the valuation.

How does AI affect the valuation of software companies?

Depending on the expected impact of AI on the business model, this can increase or decrease the company’s valuation. If AI enables faster expansion, shortens product development cycles, or opens up new applications for customers, this is a potential positive value driver. Depending on the expected impact of AI on the business model, this can increase or decrease the company’s valuation. If AI enables faster expansion, shortens product development cycles, or opens up new applications for customers, this is a potential positive value driver.