Why it usually makes no sense to negotiate with just one interested buyer when selling a company.

Time and again, entrepreneurs contact us and tell us about an offer that a potential buyer has made them. Often an initial meeting has taken place and the first documents, e.g. annual financial statements and controlling reports, have been delivered to the buyer. Now the potential buyer is increasingly requesting very specific information and the seller of the company realizes that a relatively complex and time-consuming process, including negotiations, is beginning. He seeks professional specialist support from an M&A consultancy and in some cases also considers whether he is on the right track.

It doesn’t always have to be bad to negotiate with just one company buyer. But in most cases, we will try to take a step back with our client and inform them about the consequences of such a 1:1 M&A process. Our experience has shown that it is practically always better to talk to several potential buyers at the same time and that this has very concrete, value-enhancing advantages for the seller of the company.

Competition in company sales leads to a better company valuation

Everyone knows it and many have experienced it for themselves: If you are interested in something and the seller or agent lets it be known that there are other interested parties who are very interested in the same thing, the scope for negotiations is immediately restricted from the buyer’s point of view.

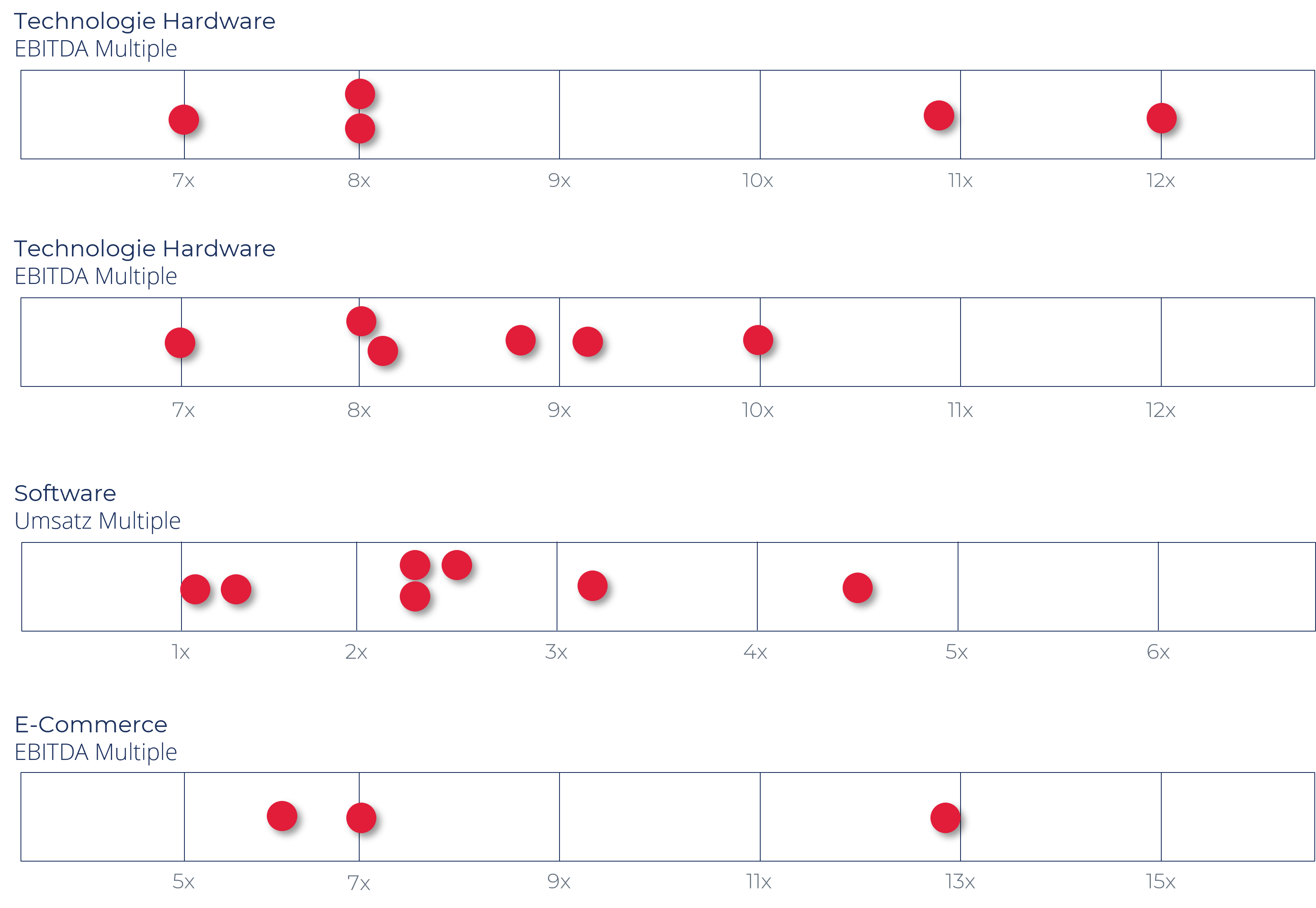

This mechanism also applies to the sale of a company. Multiple offers allow the seller to be more demanding, compare the offers and optimize their own position. In M&A practice, we repeatedly experience massive valuation differences that can amount to more than a factor of 2 between the lowest and highest offer. The following chart shows examples of such valuation differences based on real projects from the recent past. It includes the amount of the indicative offers received for so-called sell-side mandates (company sales).

Differences in company valuations from indicative offers

Examplary funnel from research to approach